If you are an estate planning attorney, CPA, or financial advisor, you likely know the basics of Qualified Charitable Distributions (QCDs). Still, you may have a hard time envisioning exactly what to say and do when they come up in a client conversation, you are not alone! Whether you are an attorney, CPA, or financial advisor, at some point you will find yourself in the middle of a QCD conversation. Here’s a case study to help you be prepared.

Margaret, a 74-year-old widow and longtime client of your practice, scheduled a meeting early in the year to discuss her charitable giving plans. In the email Margaret sent to set up the meeting, she mentioned that she was now taking required minimum distributions from her IRA and her taxable income was higher than she expected or needed.

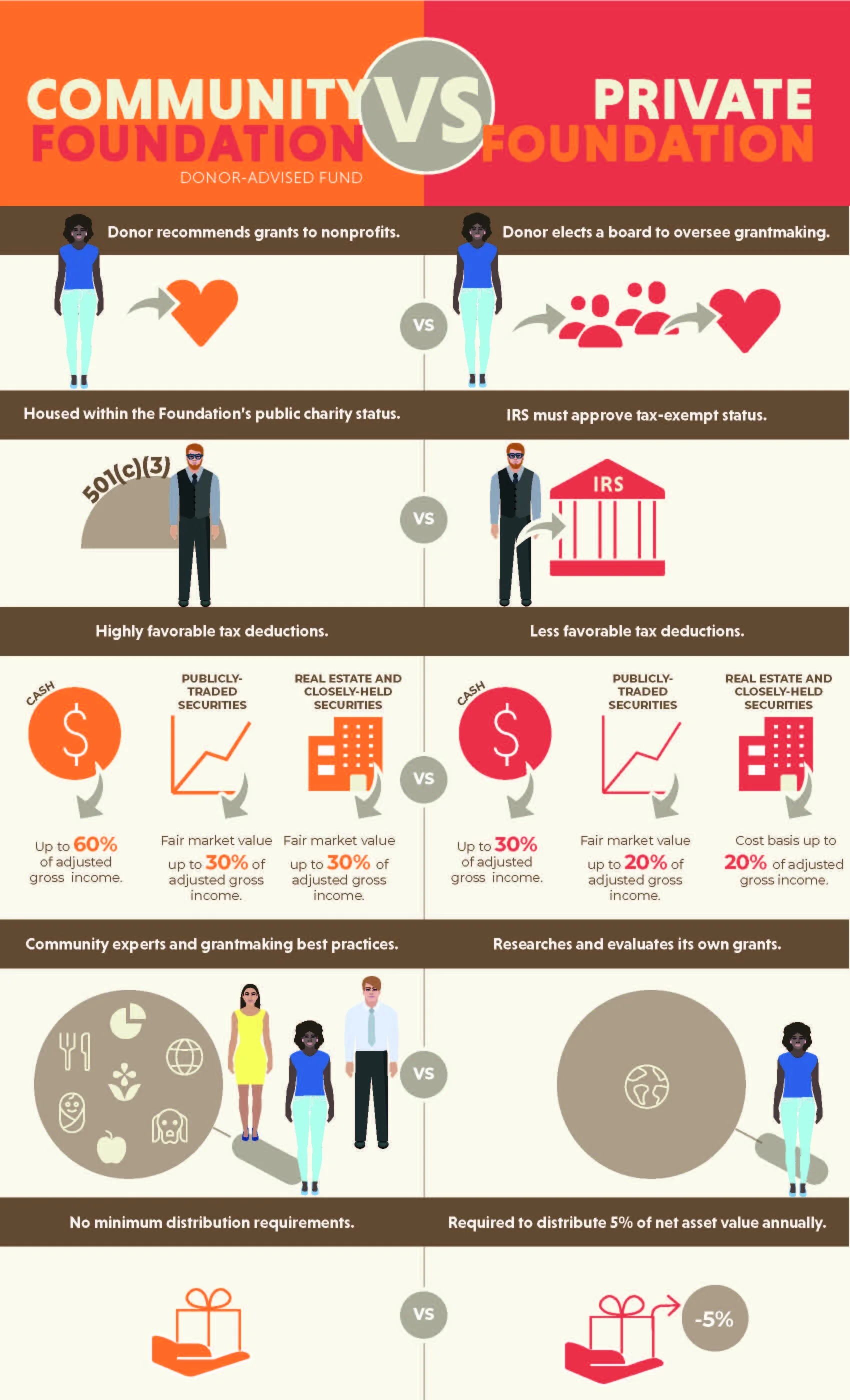

As you reviewed Margaret’s file prior to the meeting, you were reminded that Margaret had established a donor-advised fund at the community foundation several years ago. You recall from prior conversations that Margaret not only has enjoyed using the donor-advised fund to organize her charitable giving to dozens of favorite charities, but she’s also appreciated the many opportunities to tap into the community foundation’s events and educational opportunities.

Margaret arrived at your office, and after catching up on each other’s lives lately, Margaret said, “I’ve read about this thing called a Qualified Charitable Distribution. If I’m going to give to charity anyway, I want to understand whether doing a QCD in 2026 makes sense, especially if I want the gift to go through the community foundation where I already do all of my giving.”

You nod and explain that a QCD does indeed allow individuals like her who are age 70 ½ or older to transfer funds directly from an IRA to a qualified charity without including that amount in taxable income. You mention that this can be especially powerful after age 73, when required minimum distributions begin, because the QCD can satisfy all or part of the RMD while keeping adjusted gross income lower. “This can help address Medicare premiums, taxation of Social Security, and overall tax efficiency,” you continue. “With the annual QCD limit increasing through inflation adjustments to $111,000 in 2026, it’s a timely strategy to consider.”

Margaret was glad to hear all of this. Then she asked, “I already have a donor-advised fund at the community foundation. Can I simply direct my QCD straight into that fund?” You are prepared for this question! It is a common point of confusion. “That’s a great question, and you’re not alone in asking it,” you reply. “Under current IRS rules, unfortunately, QCDs can’t be made to donor-advised funds, even if they’re housed at a community foundation.”

Seeing her puzzled expression, you continue with a broader explanation. “QCDs are limited to certain types of charitable recipients,” you say. “They can go directly to public charities that are ‘operating’ nonprofits, and in limited cases to certain split-interest arrangements like a charitable gift annuity or a charitable remainder trust, subject to specific rules. Donor-advised funds are excluded, evidently because the IRS does not want the money to flow into account where the taxpayer retains advisory privileges. Donor-advised funds are of course entirely dedicated to charity, so the rule does not make a lot of sense. Yet here we are.”

Margaret frowned slightly. “That feels frustrating,” she said. “I love the donor-advised fund because it gives me flexibility and lets me support multiple causes over time.” You acknowledged her concern. “I understand. The good news, though,” you say, “is that the community foundation offers other types of funds that do qualify for QCDs and can still accomplish many of the same goals.”

You go on to explain that instead of directing the QCD to her donor-advised fund, Margaret could direct the QCD to a designated fund at the community foundation that supports specific charities she already knows she wants to help, or to a field-of-interest fund focused on causes she cares about deeply, such as education or the arts, or to an unrestricted fund to support the community as a whole. “Those types of funds are fully managed by the community foundation, without your advisory role after setup,” you say, “which makes them eligible recipients of a QCD while still aligning with your charitable intentions.”

Margaret paused, considering the options. “I don’t want to make the wrong choice,” she said. “I also want to be sure the fund is set up properly and really reflects what I care about.” You agree that is exactly the point where collaboration matters most. “This is where I’d recommend looping in the community foundation,” you say. “They can help us think through which type of fund fits best, provide a fund agreement document, and enable me to fulfill my professional duty to ensure that the structure complies with QCD rules.”

You go on to suggest a joint meeting with a community foundation representative. “The community foundation knows the nuances of the fund options and the local charitable landscape,” you explain. “That’s a great match for the legal and tax obligations on my side of the transaction. Together we can help ensure that your QCD in 2026 is clean, compliant, and aligned with your values.” Margaret smiled, clearly relieved. “That makes sense,” she said. “I don’t want this to be just about taxes. I want it to be meaningful.”

By the end of the meeting, you and Margaret have agreed on next steps: you said you would review Margaret’s IRA custodian requirements for executing a QCD, and the community foundation will set up a fund to receive the distribution. The plan will allow Margaret to use her required minimum distribution to support the community she loves, reduce her taxable income, and create a charitable structure she feels confident about.

As Margaret leaves your office, you can tell that she feels reassured that she didn’t have to navigate the rules alone. The conversation had clarified not only why a QCD in 2026 made sense for her financially, but also why working collaboratively with you and the community foundation was essential. Together, you and the community foundation can turn a confusing tax rule into a thoughtful charitable strategy that supports both Margaret’s personal financial goals and the broader community she intends to impact.

If Margaret’s situation sounds familiar, or if you anticipate any type of charitable giving conversation with a client, the community foundation is here for you! We are always happy to collaborate as you explore solutions to achieve your clients’ charitable goals. In nearly every situation, the community foundation can help. At the very least, we will point you in the right direction. Thank you for the opportunity to work together!

Pro Tip

As you talk with clients over the coming weeks, keep in mind that tax laws are always subject to change–and sometimes for the better. Case in point related to Margaret’s situation? A small, bipartisan tax law change has been proposed that would allow Qualified Charitable Distributions into donor-advised funds. Fingers crossed!

The team at the community foundation is honored to serve as a resource and sounding board as you build your charitable plans and pursue your philanthropic objectives for making a difference in the community. This newsletter is provided for informational purposes only. It is not intended as legal, accounting, or financial planning advice. Please consult your tax or legal advisor to learn how this information might apply to your own situation.